Whilst differences in local prosperity have been manifest at many points in British history, the current shape of the British economy owes much – as do so many things – to the impact of the Conservative governments of the 1980s. As David Smith put it, in his 1989 book “North and South”: “The consensus economics of the 1950s and 1960s, in which both Conservative and Labour governments undertook active Keynesian policies of demand management…..and assigned a key role to regional policy …..was willingly abandoned by Margaret Thatcher’s Conservative government……The relative decline of the North, held in check by policies deliberately designed to direct economic activity to the regions, could not survive the abandonment of such policies……or an overall economic policy stance which had as an important side-effect a second body-blow to Britain’s traditional staple industries”.

Cotton had, indeed, already gone into decline. But policies that were aimed at moving downwards the post-War “wage-share” of national income proved also to open up a new era of inequality on a national scale.

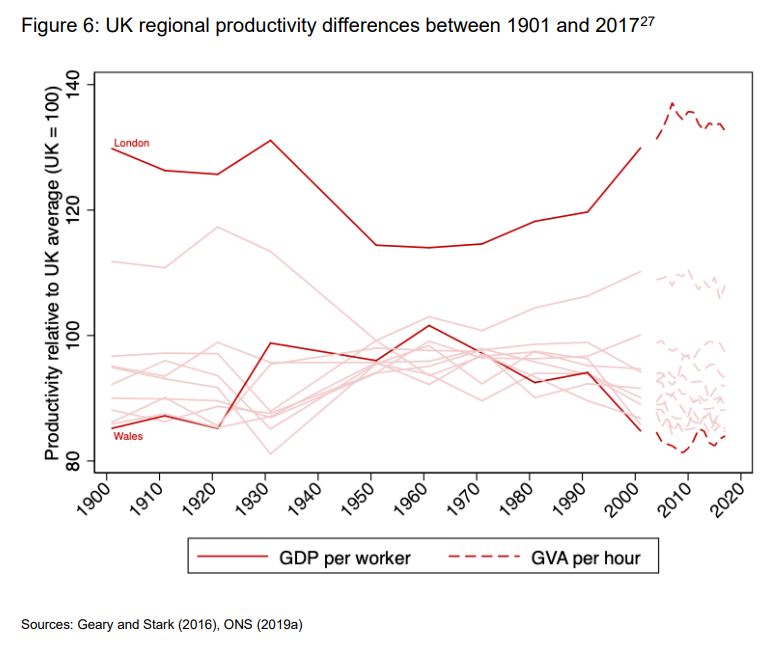

A “productivity gap” between Regions, that had narrowed since the early years of the 20th Century, began to widen again in the 1980s, alongside the decline in the “wage share” and the post-War growth in personal inequality as measured by the GINI coefficient.

The Institute for Public Policy Research Report (IPPR) “Divided and Connected – regional inequalities in the north, the UK and the developed world – state of the north 2019″(November 2019) commented: “The UK is more regionally divided than any comparable advanced economy. Our analysis finds stark regional differences in productivity, income, unemployment, health and politics. We are not the only country to have regional divides, but our regional inequalities in productivity, income and health are far worse than in any comparable country. These divides are not straightforward and they defy simplistic interpretation: the ‘North-South divide’ omits high poverty in London and the South West; the ‘cities versus towns’ debate ignores affluent towns and stagnant cities”.

In its February 2020 paper “UK Regional Productivity Differences” the Industrial Strategy Council commented that: “The magnitude of UK regional economic differences has been noted in numerous studies and reports. A 2019 article by Philip McCann of Sheffield University compares regional inequality across OECD countries by calculating a range of different indices of inequality in regional income per capita using different data sources and for different definitions of regions. Per-capita income differs from the productivity measure used throughout this document (see Box 1), but it is closely correlated. Philip McCann’s analysis reaches the conclusion that, in per-capita income terms: “the UK is one of the most inter-regionally unequal countries in the industrialised world, and almost certainly the most inter-regionally unequal large high-income country”.”

When we submitted our response to Blackburn with Darwen Council’s Local Plan review in February 2021 we noted:

“According to the “Centre for Cities” “UK Unemployment Tracker”, Blackburn had in December 2020, at 8.1%, the 9th highest percentage unemployment rate of 64 compared cities and large towns. (It is not clear if this wass for the Borough or the constituency).

According to “Lancashire Insight” the per-head figure for gross disposable household income for Blackburn with Darwen “was far below the county and UK averages. In general terms the per-head figure for the authority is in long-term decline in comparison to the UK average”. “Average earnings in Blackburn with Darwen”, “Lancashire Insight” also says, “are noticeably higher when measured by place of work in comparison to place of residence therefore the authority records a net loss from commuter flows. The figure by place of residence is well below the national average.

“The survey of personal incomes by HM Revenue and customs broadly includes all individuals whose income is higher than the prevailing personal tax allowance and who are therefore liable to tax. The median results are the middle value that best reflects typical income, and they show a result for Blackburn with Darwen that is well below the North West average”.

“The Borough has, at £25,107, one of the lowest levels of median resident earnings in Lancashire. Similarly, it sits below regional (£28,487) and national averages (£30,661).

“Our employment rate (69.4%) continues to fall below regional (72.5%) and national (76.5%) averages, though the gap has narrowed in recent years.

“We feel that our local economy has been particularly influenced by a feature that Dr Steve McIntosh called “hollowing out” in his 2013 Research Paper for the Department of Business, Industry and Skills (“Hollowing out and the future of the labour market”). This refers to the idea that local economies have lost jobs in the middle rank by income whilst the number of jobs that were the lowest paid has grown, along with the number of better-paid jobs. The September 2014 “Centre for Cities” Report “Unequal Opportunity” showed that this job polarisation affected some cities more than others. Of 59 cities compared, Blackburn with Darwen ranked 7th highest in respect of the growth of polarisation between 2001 and 2011. This finding corresponds to our anecdotal experience, in respect of the firms that we have seen disappear from round our table and in respect of seeing the churn of young people especially through precarious work positions”.

The impression given by these figures is softened a little by appreciating that regional differences between household incomes are not so wide “after housing costs” as they are “before housing costs”. And people in “prosperous” areas, on the other hand, can be just as badly off as those elsewhere – the IFS, for instance, (in “Catching Up or Falling Behind?”) points out that “after housing costs” 28% of Londoners live in poverty compared with 22% in Britain as a whole. But few people doubt that some areas remain significantly “worse off” and that this is reflected across a number of indicators. The UK 2070 Commission has stated: “The unequal pattern of economic performance is reflected in rates of employment, productivity, private investment, skills levels and the need for public subsidies. It also has been at a high cost to the UK’s wellbeing, and the pressure on public services and resources. This is unsustainable. The nature and causes of spatial inequality are problems that need to be tackled at all levels“.

Most commentators see the fundamental correlation as being that of regional differences in prosperity with regional differences in “Gross Value Added” (GVA) from different types of economic activity. GVA does have the value of identifying where there is the highest return on inputs, but it is very dependent on market outcomes and so what is being produced can be of as much significance as how it is being made. Productivity is highly correlated with real household disposable incomes at the regional level, as well as the education level of the local workforce. More productive regions also tend to have more widespread broadband access, a higher life expectancy, and a higher employment share in the local workforce.

A further correlation seems to exist between GVA and the skills/ education level of the local workforce. The Industrial Strategy Council notes: “While there is very probably a two-way relationship between local productivity and a place’s workforce skill and health, there is an overwhelming consensus that places that succeed in growing or attracting a more skilled workforce will raise their productivity. If anything, there are indications that skills have become a more important determinant of productivity over time. Research by Peter Sunley of Southampton University and co-authors has identified skills as an important driver of the divergent fortunes of British cities“.

It is also generally presumed that there must be some underlying correlation with the level of inputs available through investment and public spending. The IPPR, for instance, comment that “Comparisons have been made with German reunification – including by the government. The amount of resources invested in reducing Germany’s regional divides is considerable. On average, Germany put 70 billion euros per annum into regional development, rebalancing and levelling up-type activities – including infrastructure, education and skills, and research systems – alongside building and strengthening local institutions. This contributed to Germany outstripping the UK’s productivity growth by almost 21 percentage points between 1990 and 2017” (“State of the North 2021/22 Powering northern excellence”).

There would appear to be a gap in data when it comes to comparing investment between British Regions. The Office for National Statistics publishes information on “Business investment and gross fixed capital formation”, but does not appear to break this down regionally. The Industrial Strategy Council says: “To our knowledge, there is no high-quality data available on stocks of capital per worker across UK regions. Some evidence suggests that in the UK (as in many other countries) disparities in capital stocks mirror disparities in productivity across regions. For example, a 2011 paper by UK-based academics for the EU Directorate General Regional Policy presents experimental estimates of capital stocks per worker across NUTS2 regions in the European Union to gauge workforce access to productive assets. According to the study, capital stock per worker in the UK was highest in London, the South East and parts of Scotland, and lowest along the West Coast and the North of England”.

The UK 2070 Commission Report “Make No Little Plans” claimed that “Access to investment funding for productivity, training, innovation and improvements is crucial to business development. There are, however, questions about how well the banking system is geared to supporting local business enterprises, especially SMEs in areas such as the northern regions of England. The centralised nature of the financial system in the UK has reinforced spatial imbalances”. “Both awareness and use of equity finance remains concentrated in London and the South East. In particular, access to money for relatively small-scale and “unshowy”, but crucial investment is a major problem for many SMEs. Potentially transformative investments in equipment, technology, skills, marketing and other areas may be outside the reach of many SMEs; even £5,000 or £10,000 is prohibitive for an owner who has already made a major commitment of personal funds”.

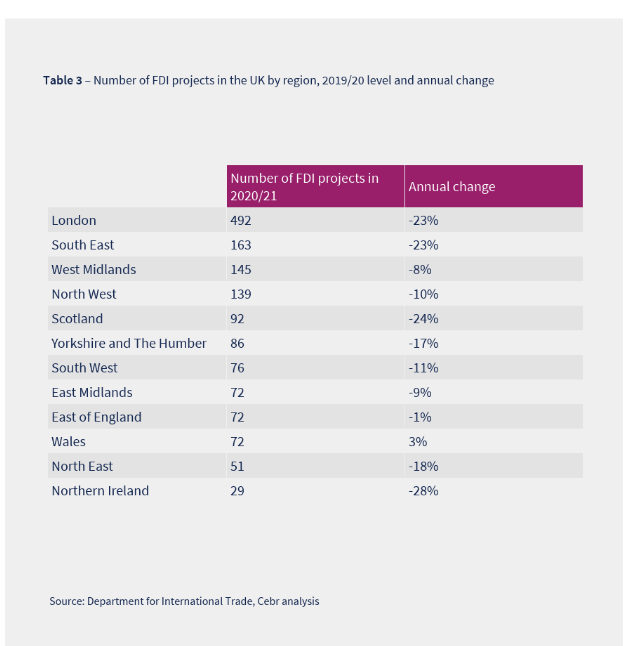

More is known about the Regional distribution of Foreign Direct Investment. Irwin Mitchell have published the following table:

which tends to support the idea that a region’s perceived attractiveness as a “place to do business” has a major influence on its ability to encourage private investments in the accumulation of productive assets. According to the Industrial Strategy Council: “A 2018 collaboration between EY and the Centre for Towns revealed large differences in the perceived investment attractiveness across UK regions. Over the last 20 years, the share of foreign-financed investment accounted for by core cities has increased from less than a third (31%) in 1997 to over half (56%) in 2017. Meanwhile, many smaller places have seen zero growth in FDI project numbers over the last two decades”.

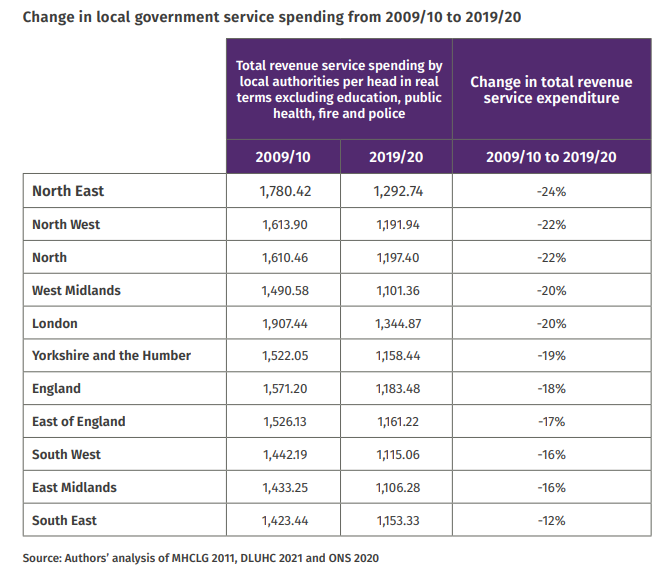

It seems not unreasonable also to believe that at least some types of public spending might have an influence over the general economic health of a locality. In different parts of Lancashire, for instance, there have been efforts to encourage big public institutions – like hospitals, colleges and local authorities – to “spend locally” in order to support local business. But if these institutions themselves become starved of money there will be a knock-on effect. For all that national Government has begun to speak more often of “levelling up”, the cuts made through “austerity” have plausibly had a stronger contrary effect. The following table, from IPPR, shows how regionally unequal the cuts to local authority spending were during “austerity”:

The IPPR commented: “…the chancellor announced £1.7 billion from the Levelling Up Fund with £0.5 billion allocated to projects in the north of England (HMT 2021). In perspective, that allocation is less than a tenth of the lost £5.16 billion in annual service spending by the North’s councils since 2009/10. That £0.5 billion is an investment of just £32 per person in the North compared to the £413 per person fall in annual council service spending from 2009/10 to 2019/20”.

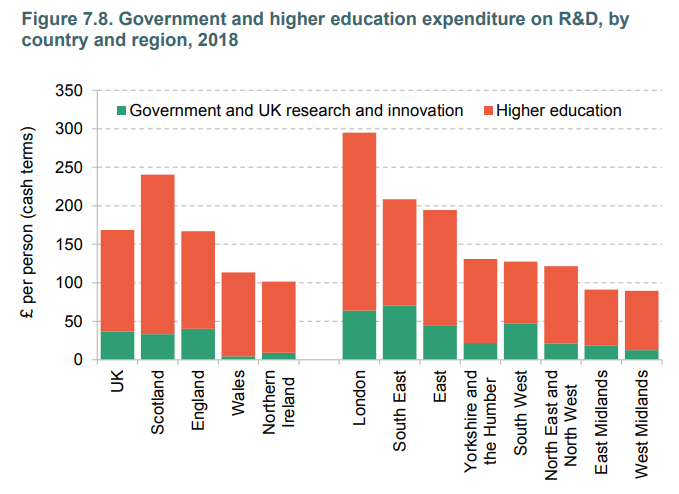

It is also known that public sector spending on R&D is spread far from evenly across the country. If one considers R&D spending by both government and higher education institutions, spending per head is highest in London (£295 in cash terms in 2018), Scotland (£240), the South East (£209) and the East of England. The following Table is from an Institute for Fiscal Studies publication “Levelling Up: Where and How?”.

On the 18th May 2022 the House of Commons “Committee of Public Accounts” published a Report on “Local Economic Growth” in which it commented that: “Despite billions spent on local growth policies over many years, the Government still does not have a strong understanding of what works. Local authorities have faced a confusion of different funding pots and have had to respond piecemeal to each new announcement over the years”. It is hard to see any strategy behind the different pots of money other than the idea that “alongside economic pull and push factors, people’s lives are shaped by the social and physical fabric of their communities”. In other words, a lick of paint in the town centre might stop everyone being so grumpy. Actually, you can’t say that this is entirely wrong – but it hardly gets to the heart of the matter when it comes to the disparity between Britain’s regions. It also seems to play the same “distraction” card so often used by Mr Johnston, in the sense that it gives Conservative MPs a chance to say “look what we are doing for you” without there being much underlying substance.

What remains missing is a determined strategy of investment to drive significant economic renewal.

Even contributors to the IMF Blog (“Public Investment for the Recovery” – 5th October 2020) have accepted that “increasing public investment in advanced and emerging market economies could help revive economic activity from the sharpest and deepest global economic collapse in contemporary history. It could also create millions of jobs directly in the short term and millions more indirectly over a longer period. Increasing public investment by 1 percent of GDP could strengthen confidence in the recovery and boost GDP by 2.7 percent, private investment by 10 percent, and employment by 1.2 percent if investments are of high quality and if existing public and private debt burdens do not weaken the response of the private sector to the stimulus”.

Jean-Marc Fournier (in “The Positive Effect of Public Investment on Potential Growth”, OECD Economics Department Working Paper No. 1347) comments that: “This paper sheds new light on the long-term effects of public investment, estimating the average effect and providing some insights on the specific circumstances, which make public investment particularly effective. The following findings emerge from the empirical analysis:

· Increasing the share of public investment in total government spending yields large growth gains.

· These gains are particularly strong for public investment in health (e.g. hospitals and their equipment) and for research and development spending…..

· The growth gains from increasing public investment may decline at a high level of the public capital stock due to decreasing returns. Still, the estimations suggest that all OECD countries, except Japan, have room for additional public investment”.

Public investment need not only be in public utilities or goods. It can also involve direct involvement in business developments. In an “Economics Observatory” article from 27th June 2022 (“What would it take to level up the UK?”) Henry Overman and Helen Simpson note: “There is evidence from the United States that attracting a large productive employer to an area can generate wider benefits (Greenstone et al, 2010). The former regional selective assistance scheme in the UK also involved subsidies to firms to locate and create new jobs in the most lagging regions. One study suggests that the scheme was relatively cost-effective in supporting employment (Criscuolo et al, 2019)” (though they do doubt for how long these effects last).

Even the Confederation of British Industry’s Director General, Tony Danker, has called for “foundational and catalytic public investments that the market will never make”. Whilst public investment alone cannot be a “quick fix” for all the ills now packaged under the “levelling up” heading, it must surely be a central component of any government’s response and a key measure of any government’s real level of commitment. We might begin to give credence to talk of levelling up when we see money coming in to set up a local Digital Catapult, or a STEM Centre at Blackburn College, or a 500+workforce new factory by the M65, or new commercial office space in the town centre. It will take not window dressing, but a tectonic shift.