January’s Trades Council meeting agreed to submit a response to the Government’s consultation on “Reforming the Right to Buy”.

Right to Buy is the scheme that allows tenants of public housing to buy the houses they rent at a discounted rate. It has been, in our view, one of the reasons why housing policy is at a point of failure across the board.

We believe that public housing at a social rent should be one of our society’s “safety nets”, available to all those who need it – with private rented and owned accomodation being available as market goods for those who are in a position to aspire to them. But many households seeking access to public housing are now denied it, at the same time as home ownership has become widely unaffordable. Many workers find themselves forced into dependence on a private sector where tenures are precarious and rents beyond their means. The “Guardian” newspaper reported on 27th December that: “nearly two-thirds of workers living in private rented housing struggle to pay their rent, according to a poll that shows how England’s housing crisis is causing financial hardship even for those with jobs”. The Joseph Rowntree Foundation published analysis in October 2021 which found that around 965,000 privately renting households in England paid more rent than they could afford. Their analysis looked at households in the bottom 40% of incomes and identified those who were either spending more than 30% of their income on rent, or who had very low residual income after paying rent.

Right to Buy has been fundamental to creating this situation, by undermining public housing for social rent to an extent that there have been harmful knock-on effects.

In October 2022 the Regulator of Social Housing said that returns from all registered providers of social housing showed that the sector owned 4.4 million homes across England.

This is about 1.1 million less than the 5.5 million available in 1979.

The proportion of social homes has fallen alongside the decline in numbers, from 31% in 1979 to about 16% now.

Neither were all of the 4.4 million homes “council houses”. Only 1.6 million units remain with Local Authority Registered Providers – most of these being in the “social rent” category.

The Government consultation on “Reforming the Right to Buy” applies only to those houses remaining in the possession of local authorities. There is a separate “Right to Acquire” affecting housing association stock, and it looks like it is intended to keep this in its current form.

Most of the research on the impact of these two “rights” has concentrated on the “Right to Buy”. It is widely felt to have been responsible for the decline in local authority owned housing for “social rent” in two ways.

A great deal of housing was transferred to housing associations mainly to protect the stock from degradation through “Right to Buy”. But large numbers of houses were also sold and not replaced. “Shelter” says: “2 million social homes have been sold via Right to Buy, with only 2% of these replaced. In the last ten years alone we’ve seen a net loss of 260,000 social rent homes with the main driver of this being Right to Buy”. Four in ten social homes sold under Right to Buy ended up in the hands of private landlords. So, homes that were genuinely affordable and secure by design have been transferred into an unregulated sector rife with insecurity and skyrocketing rents at the same time as the number of properties available for social rent has declined.

The consequences of the loss of housing for a social rent have been several.

First of all, there is simply a widespread lack of adequate provision. Almost 1.3 million households in England are on current waiting lists for social housing: More than one million households waiting for a home | Latest news | Habinteg Housing Association. Commenting on their 2021 Report “People in Housing Need”, the National Housing Association said: “there are half a million more families in need of social housing than are recorded on official housing waiting lists. This equates to 4.2 million people, including a staggering 1.3 million children”. According to “Shelter”, there are 117,000 homeless households in temporary accommodation, and there were 151,630 children in temporary accommodation at the end of March 2024. We agree with the observation made by Lloyds Bank, in their Report “Building Futures”: “Social housing is the foundation of strong communities and productive economies. Its absence exacerbates insecurity, inequality and poor health outcomes”. The “Health Foundation” say: “A secure, comfortable home enriches our lives and supports our mental and physical health. But high costs and a shortage of affordable homes means many people have to live in poor, overcrowded conditions, fall into debt because costs are too high, move frequently, or may face repossessions or evictions. This all creates instability and stress, with a significant impact on people’s health and wellbeing. In addition, strong social networks and relationships are important to our health”.

Secondly, there are fiscal costs to having an inadequate social rent stock linked to the back-wash into housing benefits and Local Authority provision of temporary accomodation. “Shelter” estimates (“Brick by Brick”) that 32% of tenants in the private sector depend on Housing Benefit/UC Housing Element to pay their rent and that spending on temporary accommodation has increased by a staggering 62% over the last five years.

Thirdly, the loss of housing for social rent has deprived the entire housing market of an important regulator. By the early 1990s, the loss of social housing was creating boom conditions for the private rental sector and the “buy-to-let” trend surged as investors purchased properties for renting, helped by banks encouraging specific buy-to-let mortgages and relatively lenient tax and regulations.. As a result, average UK house prices soared—by 2007, they had tripled compared to values in 1990, coincidentally pumping yet further demand into the private rented sector as potential new buyers began to find getting a foot on the property ladder ever more difficult. Between 1980 and 2008, house prices soared 730%. The big crash of 2008 saw another major change. Alarmed out by collapsing mortgage markets, the government introduced more strict lending rules, which made it harder to buy for the average household. There was a temporary dip in house prices, but not many were able to take advantage. Buy to Let, however, remained an attractive investment. The Buy to Let share of the market once again soared – with 2016 as the peak. House prices again began to rise faster than inflation and the return from renting was better than keeping money in the bank at rock-bottom interest rates. The process was reinforced by the consequences of QE. This, at any rate, appears to be the point advanced by “Positive Money”: “QE affects house prices through the portfolio rebalancing effect, that is, by shifting investor demand. When central banks purchase safe financial assets (such as government bonds) this provokes a reduction in their yield, making these assets less attractive for investors. This then creates an incentive for investors to “search for yield” by looking for more profitable investments such as in the residential real estate sector (IMF, 2019), which is seen by investors as a safe and attractive bet, especially in big cities (Amaral, Dohmen, Kohl & Schularick (2021). The resulting flow of money entering the property market leads to appreciating house prices. The evidence of a strong positive impact of QE on house prices has been extensively covered in the literature (Bunn, Pugh & Yeates (2018), De Luigi, Feldkircher, Poyntner & Schuberth (2019); Hülsewig & Rottmann, 2021; Lenza & Slacalek (2018); Rahal, 2016; Rosenberg, 2019“.

Years of almost continuous house price increases have driven the average home cost to 9 times the average annual earnings, a substantial rise from the 3.5 times ratio in 1997. The growth in home ownership “Right to Buy” was intended to boost went into decline: when it was launched 55% of householders were homeowners. That figure peaked at 72% in the early 00s but currently stands at 65%. According to the Commons Library Research Briefing, “Social rented housing in England: Past trends and prospects” (4 March 2024): “The Affordable Housing Commission, an independent group of housing experts established by the Smith Institute think tank, concluded: “The lack of social housing lies at the heart of the country’s affordability problem.””.

In light of the above considerations we are persuaded that an increase in the stock of social housing for social rent is necessary to both meet the immediate housing needs of many who are unlikley to have the resources to purchase property outright and to help relieve pressures that have contributed towards house purchase being so difficult.

Under the circumstances, we were bemused that the question being asked by the Government was one of whether there should be “reform” of the “Right to Buy”, rather than its complete abolition. It has already been abolished in Scotland and Wales and Northern Ireland, and whilst it might still be of benefit to some individuals this is at a continuing cost. The policy was sold as giving households a new level of security and sense of a stake in society, but its social impact has rather been to boost precariousness and alienation.

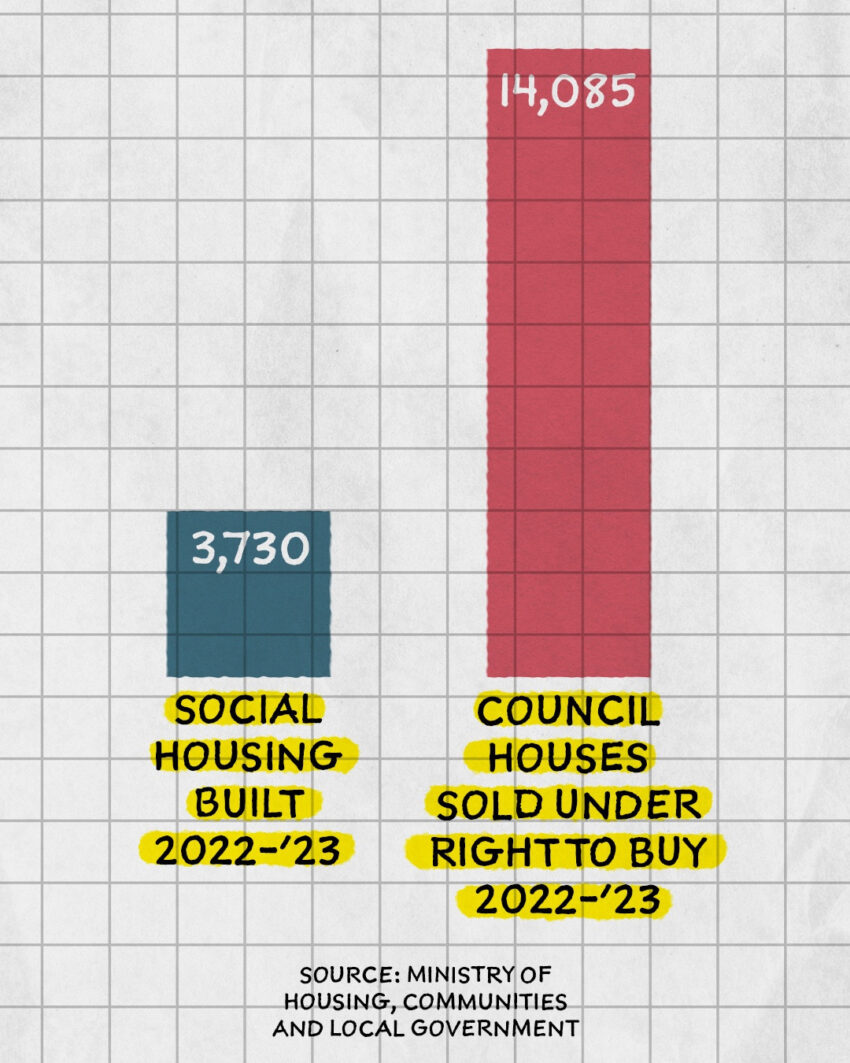

You might think that the main damage to available social housing has already been done. It looks, however, as if “Right to Buy” is still nibbling away at what is left. “Shelter” says there were 11,700 homes lost in 2022/23, and the Regulator of Social Housing said that in 2021/22 there was a “decrease in social rent units…due to losses of general needs units (14,678) offset by a 4,742 net gain of supported housing social rent units”, adding “The losses are likely to be primarily driven by sales to tenants through the various right to buy and other sales schemes”.

The proposals for reform might slow down the rate of attrition, especially if there were to be a target for all council homes sold under the Right to Buy to be replaced. Leah Milner, writing on the “Mortgage Strategy” website in October 2024, notes that sales did fall between 2004 and 2012, when the last Labour government increased the qualifying period for tenants to be able to buy their home from two to five years and also required anyone selling their home within 10 years of using the scheme to offer the property at market value back to the council or housing association that had sold it.

But what is the point of maintaining a link with the past when we need to make a completely fresh start? The reality is that even abolishing Right to Buy is unlikely, in itself, to boost to a sufficient level the number of homes available for social rent. An inquiry by the Housing, Communities and Local Government Select Committee (HCLG) into the long-term delivery of social and affordable rented housing reported in July 2020 that: “There is compelling evidence that England needs at least 90,000 net additional social rent homes a year”, whether built from scratch or refurbished. “Shelter” argues that this is a target that needs to be met 10 years on the trot. In addition the “Social Market Foundation” Report “Strong Foundations” has estimated that 380,000 social homes currently fall below the existing Decent Homes Standard, and are in need of upgrading.

If those figures are anywhere near an accurate expression of our needs it seems bizarre for us to contemplate still disposing of any public housing – and certainly not until the unmet needs have been addressed.

1 thought on “Trades Council says abolish “right to buy” and increase public housing stock.”

Comments are closed.