BT – aka British Telecom – has enjoyed the corporate equivalent of being born to the right parents. When it was privatised in 1984 it was granted a valuable inheritance from its time as a public company.

Some residual recognition that no private company could afford to build or maintain a comparable national infrastructure meant that its division “Openreach” still installs and maintains the vast network of phone line exchanges and connections into private dwellings up and down Britain, and was given responsibility for rolling out fibre-optic broadband (Virgin’s subterranean network of full fibre cabling extends to be within reach of 53 per cent of households, but tends to go where it was easiest). This “responsibility” came packaged with monopoly protection, similar to that enjoyed by the energy grid companies, and continued public investment.

The market presence and projection consequent on being still associated with the nation’s telecommunications infrastructure has undoubtedly helped BT maintain an advantageous position in terms of those functions where a market has been placed on top of the physical system. Most “providers” are actually selling you the network we have already paid Openreach to provide, though, to be fair, there is some argument that one “provider’s” broadband may be “better” than another’s in ways that do not apply to, say, electricity. You never hear anyone complain that they got EON electric by mistake last week, and it was bloody awful. But apparently broadband speeds can be affected by the technology used to ride the network.

Still, the fact that BT remains the “supplier” of an estimated 25 per cent of home broadband connections and almost 40 per cent of domestic landlines is no doubt largely down to it continuing to be seen as “the telephone company”. Neil Cumins, of broadbanddeals.co.uk comments “Many older consumers still regard BT as the default telecommunications service provider – a trusted name as newer broadband firms rebrand or get taken over”.

One would have hoped that this inheritance, and the company’s continued relationship with the state, might have given it some special sense that it had a particular responsibility to be a good corporate citizen.

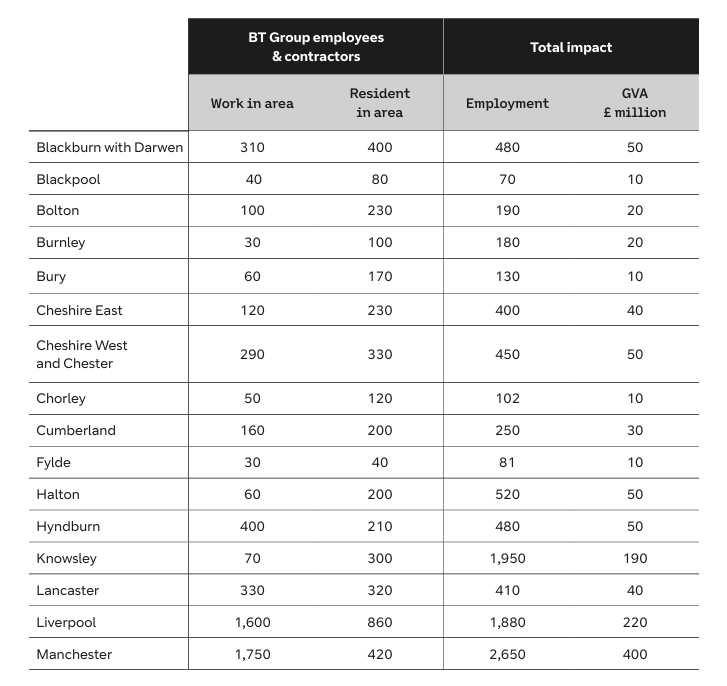

In fact, in April 2025 it did something which seemed to show that it was anxious to demonstrate this. It published an “Economic Impact Report”, prepared by independent consultancy firm Hatch, to show what a significant economic contribution the made across all parts of the country.

What seems to have prompted this was that it announced, at the same time, that it had completed its UK office transformation plan, The Better Workplace Programme, with the opening of a flagship new Manchester office: “The opening of Four New Bailey is the final step in BT Group’s five year, UK-wide ‘Better Workplace’ transformation programme, which set out to consolidate the company’s office spaces from around 300 to closer to 30 key locations” (BT completes UK office transformation plan with opening of flagship new Manchester office).

Yes, it was saying – we have closed down a lot of workplaces, but we still make an economic contribution all across the country.

The figures then given for the North West showed how important in justifying this claim were its East Lancashire operations:

Blackburn with Darwen had the highest number of BT Group employees and contractors of any location outside of Liverpool and Manchester. Blackburn with Darwen also had the third highest number of residents employed, only 20 less than Manchester.

Any credibility the company might have claimed in this respect it has now entirely trashed with the announcement that it is going to close its operations at the Globe Centre in Accrington and the “Telephone Exchange” building in Blackburn.

This despite having announced that the “Better Workplace Programme” had been completed, and despite all previous discussions around the future of these sites having concentrated on questions of potential merger or refurbishment.

A Report on “TelcoTitans” on 30th April 2025 – “Better Workplace: BT closes out five-year real estate overhaul programme” (Better Workplace: BT closes out five-year real estate overhaul programme | Operations | TelcoTitans.com) – incorporated a Table of “BT’s Better Workplace offices, April 2024”, citing BT as a source and saying that the “locations listed are those known to be included in the Better Workplace programme”. Accrington appeared at the top of this list.

Mustafa Faruqi, BT Group Employee Relations Strategy Director, tells us that: “We….understand why this announcement may have come as a surprise, particularly in the context of previous communications about BT Group’s estate and recent publications highlighting our economic contribution. However, the proposals affecting Blackburn and Accrington are the result of a detailed, site specific review…”, and “whilst the Better Workplace Programme has concluded nationally, our estate strategy continues to be reviewed as business needs, working patterns and utilisation evolve”.

In other words, this is a company that undertakes a major, 5-year spatial re-organisation and then turns round and says “oops, missed a bit”.

We expect better from a business whose relationship with our country is as we have described. The CWU Lancashire and Cumbria Branch has produced a counter-proposal that has won the support of local politicians and which we have urged the company to accept.

These closures come at a time when the “Centre for Cities” Report “Cities Outlook 2026” notes that “on average, London residents (£27,200 per person) have almost twice the disposable income (before housing costs) than residents of Blackburn (£15,200 per person)”, and “in Blackburn, the city with the lowest disposable income per head, the majority of neighbourhoods – 56 per cent – are among the most income deprived in the country”. In Blackburn, not a single income deprived neighbourhood in 2010 had escaped that status by 2025.

The “Telephone Exchange” closure will be a particular blow to Blackburn’s town centre economy. We have in several circumstances made the case that town centre employment is a vital part of maintaining vibrant town centres.

The circumstances would not be so bad if we could anticipate compensating investment. Germany invested some €70 billion per annum for 30 years in “levelling up” the East and West following reunification. Where is our reunification?